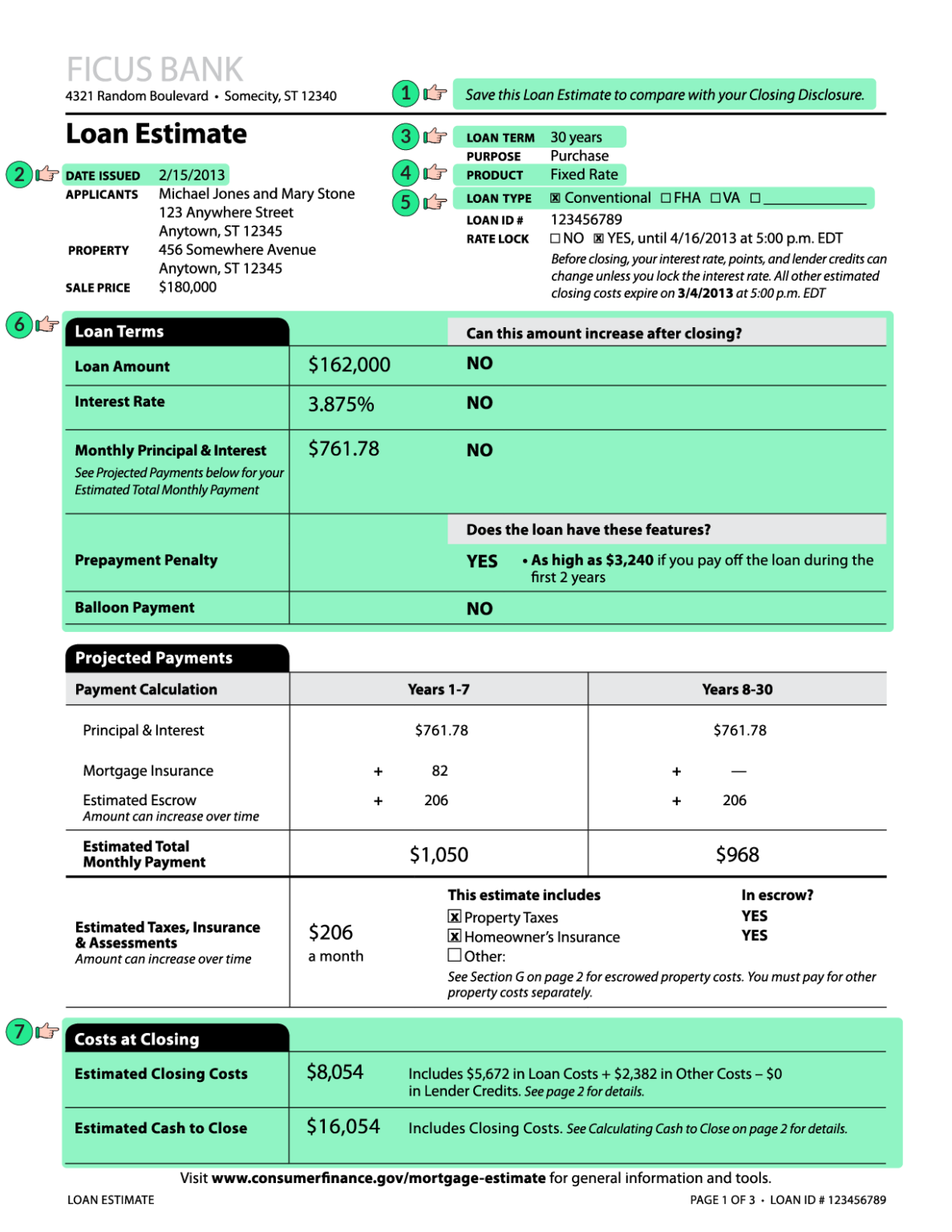

Unit selection Mortgages are in a range of terms

To own „examine will cost you over the amount of ages?” suggest the period of time you expect to own your property. Make use of the incrementer at the end of the field to include otherwise deduct years. Since you do, observe that the new calculations presented to suitable changes because you include or subtract ages.

Optionally, render a great guesstimate regarding how you feel can happen in order to home values across the time period you registered into the „contrast costs more banks near me for personal loans no credit history than what amount of age?” Getting reasonable-deposit home loan products that wanted PMI, home price really love normally speed up the amount of time it will require to arrive at a time where you could cancel particularly an insurance policy, slicing your monthly financial costs.

Getting a most direct testing, please favor a credit rating „bucket” that is closest towards score you may have

Today, compare FHA will cost you up against another prominent choice on the market, „Conventional 97” (3% down) investment. About container towards the bottom, where it says „Should evaluate FHA against almost every other lowest down payment mortgage solutions?” mouse click „Yes.”

Antique 97 mortgages need just step 3 per cent off and they are offered with no special restrictions all across the country. Yet not, low advance payment mortgage loans carry alot more risks into the lender, and higher threats is also getting higher will cost you, particularly when a debtor have a faster-than-perfect credit rating. In the event the credit is right but your ability to cut back an advance payment is restricted, a normal 97 mortgage will be useful for you.

As opposed to the lowest-advance payment FHA home loan, Antique 97s explore antique PMI procedures; these may feel terminated at the a future date after the financing seats a keen 80% loan-to-really worth (LTV) ratio. This occurs on the next intersection regarding paying down brand new loan’s the balance and exactly how rapidly the worth of your residence goes up. PMI cancellation is often as absolutely nothing since the 2 yrs aside.

Comparing HomeReady and you may House You are able to mortgagesAimed at reduced-to-moderate income buyers or geared to unique geographical towns and cities is easily finished on the website. HR/Horsepower mortgage loans accommodate simply a beneficial step three per cent down-payment however, such finance keeps reasonable or no chance-based premium you to definitely drive up financial will set you back, thus qualifying individuals can find these types of since the affordable while the FHA-supported loans. Unlike the new FHA program, even in the event, Time and you will Hp mortgages support PMI getting terminated at another area, so home loan will cost you could be lower in the near future.

Interest The fresh new loan’s interest rate. You can expect the common compliant 31-seasons fixed-price financial (FRM) interest as the a starting point; this really is altered as needed. The interest rate ‚s the key used by the loan percentage calculator to see which your own payment and you will can cost you will end up being over the years.

Deposit Having investigations intentions, the brand new calculator allows four prominent different choices for step three.5%, 5%, 10% and you will 15% off. The available choices of a little advance payment is the hallway, and in case a debtor puts 20% down or higher, PMI is not required having conventional mortgage choices, so there might be nothing to examine an enthusiastic FHA mortgage facing.

Fund upwards-front MIP? (Mortgage premium) The brand new FHA system requires payment regarding an upwards-side payment, currently 1.75% of the loan amount.

Fixed-price mortgage loans are most often included in 31, 20, 15 and you will ten-12 months words; changeable rate mortgages often have complete regards to 30 years, however the repaired interest rate period is much reduced than you to definitely, long-lasting from so you can 10 years. The fresh dropdown right here enables the option of FRMs having terms deeper or less than twenty years, and three prominent crossbreed Case terminology.

Credit history As FHA system will not use chance-built rates, hence increases charges for consumers that have lowest credit score, low-down payment applications one a borrower can certainly be finding carry out use them.